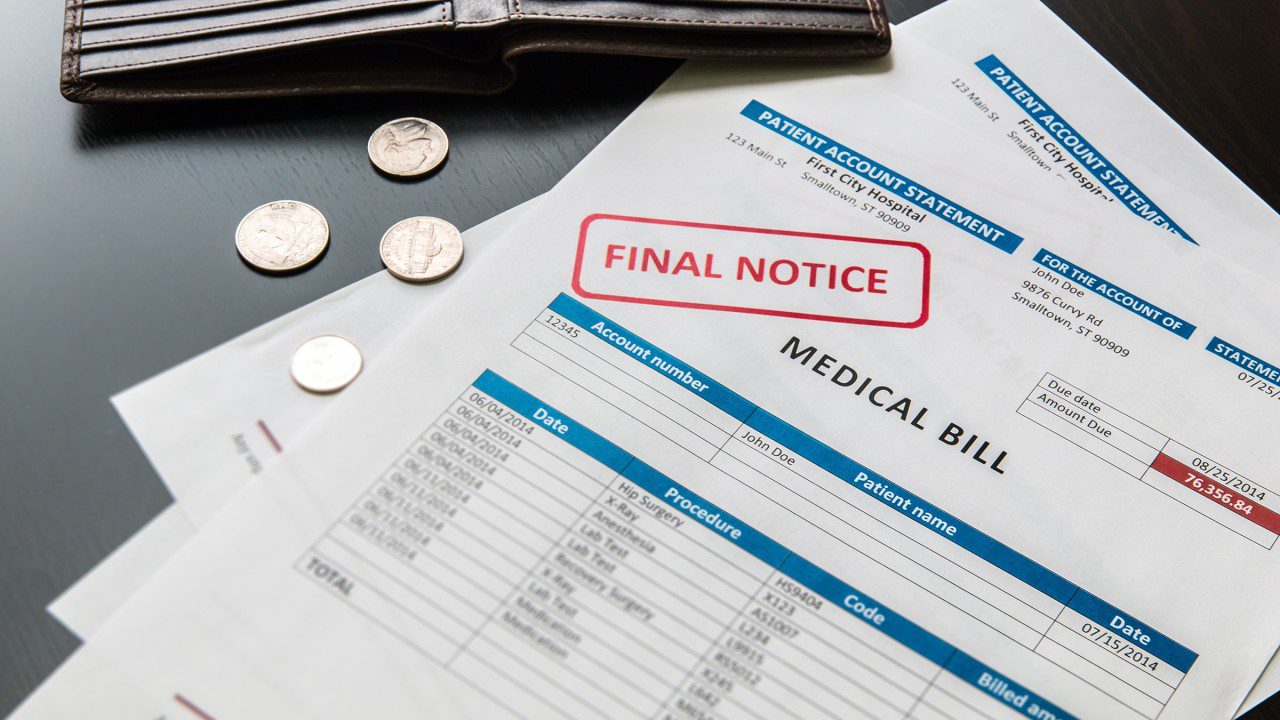

Medical emergencies can make a person emotionally and physically stressed, and they medical emergencies come with other stress, such as medical bills. Whether it is an unexpected surgery, ongoing treatment, or hospital visit, the costs can increase quickly. One question that comes to everyone’s mind is “Do Medical Bills Really Affect Your Credit History?”. The answer to this question is yes, medical bills can affect your credit history. But how, when, and to what extent medical bills can affect is more complex.

This comprehensive guide will let you know everything about the impact of medical bills on your credit. You will get to know how certain changes in the credit reporting can affect this, and what the main steps are to be taken to protect your financial health.

According to a study from 2021 from the Consumer Financial Protection Bureau, approximately 1 in 5 Americans has some form of medical debt. The total amount of medical debt in the U.S. is estimated to be around $88 billion. Around 58% of collections on consumer credit reports in the U.S. are related to medical bills (as of 2021).

Table of Contents

Comprehensive Guide: How Credit History Works

Before diving into the other aspects of medical bills, you need to understand what a credit history is and how it works.

Credit History: Credit history is a record of how you have managed your loans, credit cards, and other forms of debt. In the medical history, some factors are involved, including:

- The number of credit accounts you have

- Your payment history

- Amount of debt owed

- Length of credit history

- Types of credit used

- Recent credit inquiries

Do Medical Bills Show Up on Your Credit Report?

Medical bills do not show up on your credit report directly. Medical providers don’t report to credit bureaus at all. The story changes if you don’t pay those bills over time. How does this process actually work? Let’s understand:

- You will receive a medical bill directly from a hospital, doctor, or lab.

- Many providers offer payment plans or financial assistance if you want. You will be given the time to pay or negotiate.

- If your bill remains unpaid, the bill may be sent to collections. This process happens after 90-180 days of non-payment.

- Once your bill is sent to collections, it may be reported to credit bureaus. After showing up on your credit report, and starts affecting your credit score.

New Rules: Changes in Medical Debt Reporting

New rules and significant changes are implemented in how they handle medical debt. As of July 1, 2022, three major credit bureaus- Equifax, Experian, and TransUnion implemented new rules that can help reduce the impact of medical debt on consumer credit reports. Here are the changes in the medical debt reporting:

1. Paid medical collections are no longer reported

Your medical bills don’t appear on your credit report if you have paid off the medical collection account.

2. One-year grace period before reporting

After the medical debt goes to collections, medical debt will not be reported for at least 365 days. This timeline can help you work with the healthcare providers or insurance companies to resolve the debt.

3. Smaller balances removed

Starting in 2023, medical debt under $500 is excluded from your credit report, even if unpaid.

These updates act as game-changers because:

- They protect consumers from the unexpected medical expenses that damage their credit.

- These changes give time to sort out the billing errors or insurance claims.

How Medical Debt Affects Your Credit Score

If your medical debt does get reported, it is treated similarly to other types of debt in collections. A collection account can damage your credit score, especially if you had a good score to begin with. FICO and VantageScore are the two main scoring models that have made updates to reduce the medical collections weightage.

- FICO 9 and FICO 10 scoring models weigh medical collections less than other types of collections.

- VantageScore 4.0 completely ignores paid medical collections and puts less emphasis on unpaid medical debt.

- Some lenders still use older scoring models, so the impact can vary depending on the lender.

Should You Ignore Medical Bills?

No, it is not an ideal thought to ignore medical bills. Ignoring medical bills can lead to legal actions. Here are some reasons why you should not ignore the medical bills:

Debt collectors may take legal action:

If a collection agency wins a judgment against you, it can place a lien on your property. After winning a judgment against you, they can garnish your wages.

Interest and fees may accumulate:

- If your credit is not impacted immediately, late fees and interest can balloon your original bill.

- They can still end up in Collections

- If the collections remain unpaid, medical bills can be sold to debt collectors. If this condition happens once, your credit score can take a hit.

How to Prevent Medical Bills from Hurting Your Credit

Some practical steps that can be taken to prevent medical bills from hurting your credit and protect yourself. Below are the steps you can follow:

- You need to review all your medical bills carefully. Check for the errors. Medical billing mistakes are common, and you may be charged for services you didn’t receive or that were covered by insurance.

- You can communicate with the providers if you can’t pay in full. Ask for payment plans, financial assistance programs, and charity care.

- If you offer to pay a portion upfront, many medical providers are open to reducing the bill.

- Delays in the insurance processing can cause bills to be sent to collections. You need to make sure your insurance provider has all the essential documentation they require.

What If You Already Have Medical Debt on Your Credit Report?

If you already have medical debt on your credit report, you need to follow some steps, including:

- The first step is to check if it is already paid. If it’s paid and still showing on your report, you can contact the credit bureaus to have it removed.

- You can request validation under the Fair Debt Collection Practices Act (FDCPA). If they can’t validate the debt, they must remove it.

- Negotiate a Pay-for-Delete. When you offer to pay the debt in exchange for having it removed from your credit report. Not all collectors agree to negotiation, but it is worth trying.

- Seeking professional help can be a good idea. Reach out to a nonprofit credit counseling agency for appropriate guidance on managing your debt without damaging your credit.

Final Thoughts: Protect Your Health And Your Credit

- Medical bills can be overwhelming. These medical bills don’t have to destroy your credit. Recent changes for medical debt have offered more time and options to address bills before they affect your financial future. You need to be open to medical billing and read it carefully.

- Read medical bills properly.

- Don’t delay in addressing medical bills.

- Monitor your credit report for any unexpected entries.

How do we help healthcare professionals get their Medical Claims paid?

TueCa RCM™, LLC is a trusted medical billing partner of healthcare professionals when it comes to medical billing. The team at TueCa RCM™ brings the experience of over 24 years in handling medical billing and client relations. Our personalized approach and attention to detail can minimize claim denials and ensure prompt reimbursement from payers. Our experts can manage accounts receivable the improve cash flow for the healthcare practices. We can conduct follow-ups with payers and resolve the claim denials. With our expertise in revenue cycle analytics, we can offer valuable insights that can enhance the collection efforts and reduce outstanding balances.

Contact us at https://carelinkbillingservices.com/ to know more about the Medical Billing Service we offer. You can email us at info@carelinkbillingservices.com and call or text us at 307-222-1189.

FAQs About Medical Bills and Credit History

Question 1. Can unpaid medical bills affect a credit score?

Answer. Yes, unpaid medical bills can affect a credit score. This can happen if the medical bills are sent to collections and remain unpaid for over 12 months. If the bills are once shown in collections, these can also appear on your credit report and lower your credit score.

Question 2. How long before medical debt shows on your credit report?

Answer. The current rules say that medical debt won’t appear on your credit report until it has been in collection for at least 12 months. This period allows time to resolve insurance claims or billing issues.

Question 3. Can I dispute medical bills with the credit bureaus?

Answer. You can dispute it with the credit bureaus if a medical debt shows up on your credit report in error. To dispute incorrect medical bills, you need to provide documentation proving the debt is invalid or paid already.

Question 4. Can I ignore medical bills?

Answer. No, you should not ignore medical bills. Recent changes for medical billing are consumer-friendly, but it is not an ideal choice to ignore the medical bills.