How to Remove Medical Bills from Your Credit Report Legally: Medical bills can be a source of stress, especially when they appear on your credit report. Medical providers must figure out how to manage these bills so that it does not impact their patients with bad debt. This blog will discuss how medical bills can appear on your credit report, how to get them taken off legally, and how TueCa RCM™ can assist medical providers in bill payments.

Table of Contents

What Is Medical Debt on Your Credit Report?

Medical debt can have a serious impact on your general finances. A bill not paid on time could go to collections and subsequently impact your credit score. Luckily, there are specific ways to address bills sent to collections for medical purposes and ensure they are done legally and sufficiently.

Medical bills are generally treated differently from other forms of debt. The way to manage medical bills and debt proceeds along similar but different processes if you are a healthcare provider managing patients who will be dealing with medical costs, specifically medical debt. Processes for managing medical fees usually become debt collection after a bill is more than a couple of months late. It does not mean that if a patient has insurance, but the claim is still being processed that the bill will remain unpaid simply because there is no response from the claim.

For independent healthcare providers, small practices, and clinics, understanding the proper way to deal with unpaid medical bills is important for both your patients as well as your practice.

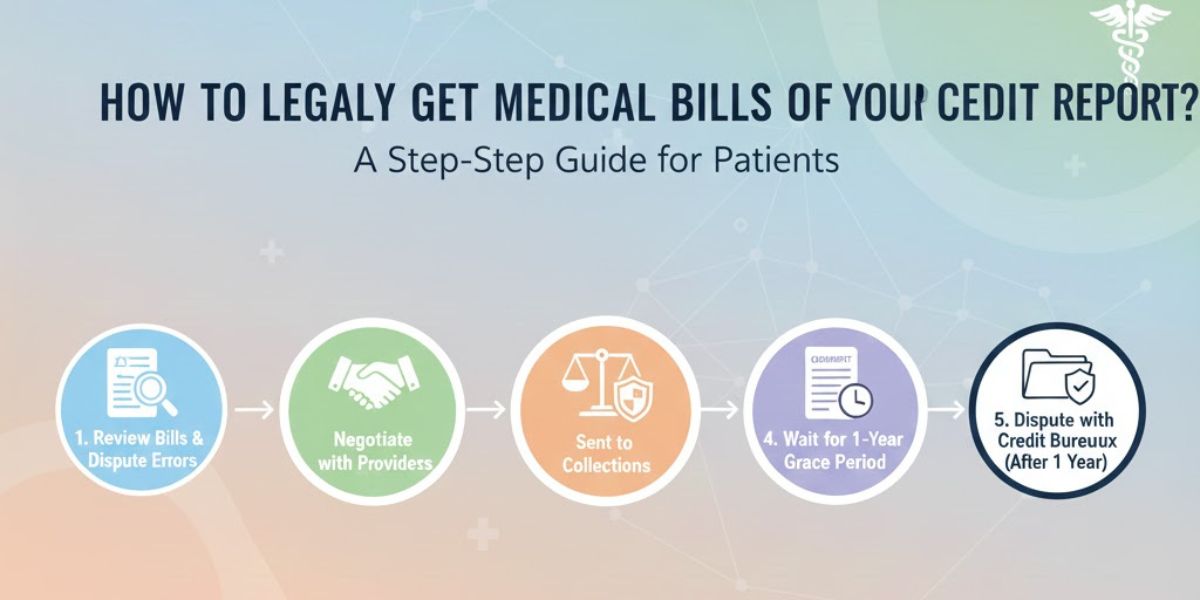

How to Legally Get Medical Bills Off Your Credit Report?

Removing medical bills from a credit report can be a difficult task; however, there are ways to legally remove medical bills from a credit report:

Step 1: Review Your Credit Report for Accuracy

The first step in removing any medical bills from your credit report is to review your credit report for accuracy. Request a free copy of your credit report from one of the three main credit reporting agencies: Experian, Equifax, or TransUnion. Review the copy of your credit report for any medical debt that shouldn’t be reported on the credit report (i.e., incorrect charge or outdated debt).

As a healthcare provider, you need to make sure that all claims are submitted, coded correctly, and paid in full by the insurance company. Errors in coding or billing, or unprocessed payments, will end up on the patient’s credit report.

Step 2: Documentation with Creditor

If you come across medical debt that you believe to be inaccurate or incomplete, make sure to check the documentation with the creditor or collection agency. Confirm that the medical bills were processed correctly and that the insurer handled all claims in accordance with the patient’s policy. Sometimes, insurers incorrectly deny claims that are owed, or payments may be tied up, leading to excessive waiting periods, thus penalizing patients unnecessarily.

If you are a certified independent provider, it is important to keep accurate records and coding to minimize such mistakes.

Step 3: Dispute inaccuracies with the credit bureaus

If you find inaccuracies or non-validated medical bills on your credit report, then it is within your rights to dispute these items with the credit bureaus. The credit reporting bureaus have a legal obligation to investigate the disputes and remove any inaccuracies found. Be prepared to offer supporting documentation, including the office’s records showing the claim was paid or showing the amounts billed are incorrect.

Step 4: Negotiate with creditors or collection agencies

If the debt is valid and sent to collections, you can negotiate with the collection agency to refresh the record and wipe the debt completely in exchange for a payment. This is called “pay for delete”.

Not all collection agencies will agree to remove the debt after payment. Be careful and make sure to get this in writing before you pay.

Step 5: Request a Goodwill Adjustment

Even though not always guaranteed, in some cases, you can ask the creditor/collection agency for a goodwill adjustment. If the medical debt resulted from financial hardship, the agency might agree to remove the debt from your credit report as a goodwill gesture. This will be especially effective if the patient has typically made timely payments and only has this one instance of a relation to the debt.

Step 6: Wait for the Debt to Drop Off

If you’re not able to resolve it immediately, most medical debt will fall off of your credit report after seven years from the first missed payment date. While this isn’t the ideal process if you are trying to improve your credit score in the meantime. If the debt exceeds the statute of limitations, the creditor cannot sue to collect, but the debt may still show up on your credit report.

How TueCa RCM™ Can Help?

As an independent healthcare provider, small practice, or clinic, it becomes difficult to manage billing, coding, and revenue cycle management, especially when the errors cause unpaid medical bills that can affect the patient’s credit. TueCa RCM™, LLC, is committed to helping healthcare professionals. We can help you in several ways, including:

- Proper Coding and Billing: TueCa RCM™ strives to ensure that all medical coding and medical billing are accurate on the first attempt. This reduces the possibility of inaccuracies that could produce unrealized collections or wrongly submitted billing to a collections agency.

- Quicker Reimbursements: TueCa RCM™ will also help you receive quicker reimbursement from insurance companies and decrease the likelihood of unpaid bills being sent to collections, sparing you and your patients from the negative implications of medical debt on their credit report.

- Compliance: TueCa RCM™ monitors healthcare industry regulations and ensures that all billing and coding is compliant with current regulations, reducing your chance of collections being rejected or being penalized as a provider, and protecting the patient.

- Debt Collection Help: If a patient has a history of unpaid bills, TueCa RCM™’s team can assist you in efficiently providing collections for those debts. Our support will always be in a professional manner that complies with local laws.

- Patient Friendly: We believe in assisting your patients, as well. TueCa RCM™ helps your patients understand their situation in regard to their medical bills. Our goal is to ensure that your patients understand their obligations, which reduces the possibility of disputes that could lead to unpaid collections on their credit report.

![]()

Conclusion

Navigating medical debt can be challenging, but you can legally remove medical bills from your credit report. Dispute erroneous information on your credit report, and collaborate with your patients’ creditors to help restore a better payment history, thus improving your patients’ credit scores, and supporting healthier revenue cycle performance for your practice. TueCa RCM™, LLC, is here to partner with healthcare providers for accurate billing, compliance, and the continued financial well-being of your patients. Let us handle the billing and ensure your patients’ financial recovery while you focus on your patients.

Frequently Asked Questions:

Question 1: Can I remove medical bills from my credit report after they’ve been sent to collections?

Answer. Yes, you can remove medical bills from your credit report by disputing errors, negotiating with collection agencies, or requesting a goodwill adjustment. Ensure that you have documentation to support your case.

Question 2: How long does it take for medical debt to drop off my credit report?

Answer. Medical debt typically stays on your credit report for up to seven years from the date of the first missed payment. After that, it will automatically be removed.

Question 3: Can TueCa RCM™ help me avoid billing errors?

Answer. Of course! TueCa RCM™ ensures that all billing and coding are accurate, minimizing the risk of errors that could lead to unpaid bills or negative impacts on your patients’ credit scores.

Question 4: Can I negotiate a lower payment for my medical debt?

Answer. Yes, you can negotiate with creditors or collection agencies to reduce the amount owed or set up a payment plan. This may also include negotiating for a “pay for delete” arrangement, where the debt is removed from your credit report after payment.