Medical Debt is one of the most common type of debts and causes of bankruptcy in the United States. Millions of people across the country accrue medical debt from unexpected hospital stays, emergency procedures, and even routine healthcare visits can leave people facing unmanageable bills. If you are struggling with medical debt, you are not alone and you certainly have options.

If you have unmanageable medical debt, bankruptcy can be a powerful tool to help you regain financial control. Whether you are thinking how unpaid medical debt can affect your credit score or exploring legal options for relief, understanding your rights and legal option is important. In this blog, we will understand medical bills and debt and how bankruptcy may be your best option to make life affordable again.

Table of Contents

Overview of Medical Debt Situation in USA

Medical Debt has become a national crisis. Recent studies have shown that more than 100 million Americans have some form of medical debt. Many of these families are struggling to pay insurance and healthcare expenses. Unlike other types of debt, medical debt is often unexpected, leaving families without a financial planning to manage it.

For years, medical costs have continued to rise and create an unmanageable burden for people and families across America. Many people are forced to choose between paying the medical bills and covering essential living expenses like rent, groceries, or utilities. As a result, unpaid medical debt remains one of the leading causes of bankruptcy in the United States.

What Happens if I Don’t Pay the Medical Debt?

When medical bills remain unpaid, they don’t just disappear. Healthcare providers usually attempt to collect payments directly at first by sending reminders and notices. If those attempts fail, they may transfer the debt to a collection agency.

Once a medical bill is in collections, you may receive persistent calls and letters from debt collectors. This can lead to increased stress and anxiety, making an already difficult situation worse. If the debt remains unpaid for more than a year, you could face additional consequences.

Ignoring medical debt can have long-term financial implications. However, there are ways to address it before it spirals out of control. Understanding your rights and the options available can help you navigate the situation effectively.

Medical Debt Collection Laws

Understanding medical debt collection laws can help you protect your rights and prevent unfair practices. Its important to understand the statute of limitations for medical debt and the Fair Debt Collection Practices Act.

Statute of Limitations for Medical Debt

Each state has a statute of limitations on medical debt which is the time period in which a creditor can sue you for unpaid bills. This period typically ranges from 3 to 10 years, depending on the state. Once the statute of the limitation expires, debt collectors can still attempt to collect, but they can no longer take legal action against you.

It’s important to check your state’s laws and be aware of any legal time limits on medical debt. If a collector tries to sue you for an old medical bill that has passed the statute of limitations, you may have legal grounds to challenge the case.

Fair Debt Collection Practices Act

The Fair Debt Collection Practices Act (FDCPA) is a federal law that protects consumers from abusive debt collection practices. Under the FDCPA, debt collectors are prohibited from harassing you with excessive phone calls, threatening you with jail time, contacting you at unreasonable hours, or misrepresenting the amount you owe.

If a debt collector violates these rules, you have the right to take legal action. Knowing your rights under the FDCPA can help you stand up against unfair collection tactics.

Bankruptcy and medical debt

For people who feel overwhelmed by medical bills, bankruptcy can provide a fresh start. While bankruptcy may seem intimidating, it’s a legal tool designed to help individuals regain financial stability.

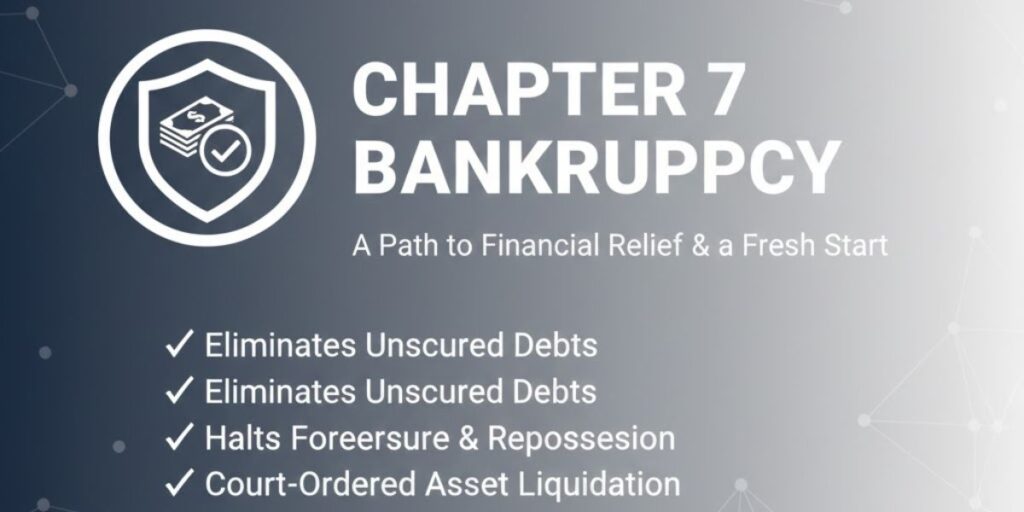

Chapter 7 bankruptcy due to medical debt

Chapter 7 bankruptcy is the most common form of bankruptcy for those dealing with large amounts of medical debt. People can utilize Chapter 7 bankruptcy to discharge unsecured debts, including medical bills, in a relatively short period—usually within three to six months.

However, to qualify for Chapter 7, you must pass a means test, which evaluates your income level. If approved, most or all of your medical debt could be discharged, giving you a fresh financial start.

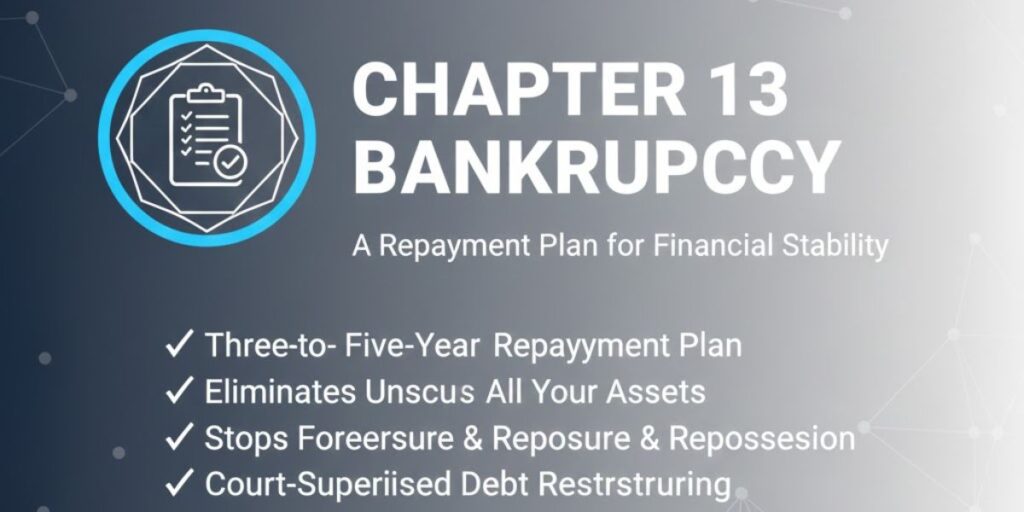

Chapter 13 bankruptcy due to medical debt

If you do not qualify for Chapter 7 or want to keep more of your assets, Chapter 13 bankruptcy may be a better option. Chapter 13 creates a structured repayment plan that allows you to pay off your debt over 3 to 5 years.

With this approach, medical debt is combined with other debts, and a manageable monthly payment is established based on your income. Once you complete the repayment plan, any remaining medical debt may be discharged.

While Chapter 13 takes longer than Chapter 7, it can be a good option for people who want to keep their property and address their financial struggles.

Final Thoughts

In 2025, medical debt continues to be a major source of financial hardship, especially for Californians facing rising healthcare and living costs. Bankruptcy can offer a legal and effective way to regain control, but it is not a one-size-fits-all solution. By learning more about your options and consulting with a trusted professional, you can take the first step toward financial relief and peace of mind.

If you are weighed down by medical bills and unsure where to turn, know that help is available. Understanding your rights and the potential role of bankruptcy may be the beginning of your financial recovery.